Iran War Weighs on Global Markets

Conflict in the Middle East has unsettled markets, driving volatility and raising concerns over inflation.

Energy shock clouds the outlook.

The Iran war has created fresh uncertainty for the global economy, complicating efforts by central banks to contain inflation. Its effects have rippled across markets, fuelling volatility and clouding the outlook for growth.

Wholesale oil and gas prices have surged, with experts warning that if prices remain elevated, goods and services could become more expensive. The extent of any rise in inflation will depend on how long the conflict lasts and when tankers can pass through the Strait of Hormuz again.

Global equities have come under pressure and bond yields have risen. Despite this, US stocks have held up relatively well, supported by solid earnings and economic resilience. Central banks are now expected to keep interest rates higher for longer, with the possibility of further increases if price pressures persist.

Soaring fuel costs have also weighed on the US economy. Gasoline prices hit $4 a gallon, their highest since 2022, undermining President Donald Trump’s claims to be tackling the cost of living. Labour market data has weakened, with payrolls falling by 92,000 in February and unemployment rising to 4.4%.

With volatile oil prices and weaker job data, the US Federal Reserve (Fed) held interest rates steady at its March meeting. US inflation remained at 2.4% in February, ahead of the energy shock triggered by the conflict.

Bank of England holds rates.

The Bank of England kept interest rates at 3.75% amid growing concern over rising energy prices. As a major energy importer, the UK is exposed to higher oil and gas costs, which threaten efforts to bring inflation back to its 2% target. Inflation held at 3% in February, with increases likely in the coming months.

The UK economy slowed in January, even before the latest energy price rises. Growth was flat, following a 0.1% increase in December. The unemployment rate rose to 5.2% in the three months to January, while earnings growth also eased.

China's economy rebounds.

China's economy showed signs of recovery in early 2026, supported by stronger factory activity, consumption and investment. Large oil reserves and a shift towards renewables should help cushion the short-term impact of supply disruptions. However, a prolonged conflict would increase the economic cost.

China set a growth target of 4.5% to 5%, the first time it has fallen below 5% since 1991, reflecting structural challenges, including the property downturn.

In Europe, the European Central Bank (ECB) kept interest rates at 2% for the sixth consecutive meeting as inflation rose to 1.9% in February. Higher energy prices could push inflation above target and weigh on growth in the coming months.

It is important to remember that while geopolitical shocks can trigger short-term volatility, history shows markets tend to recover over time. We will continue to monitor developments closely and adjust our views accordingly.

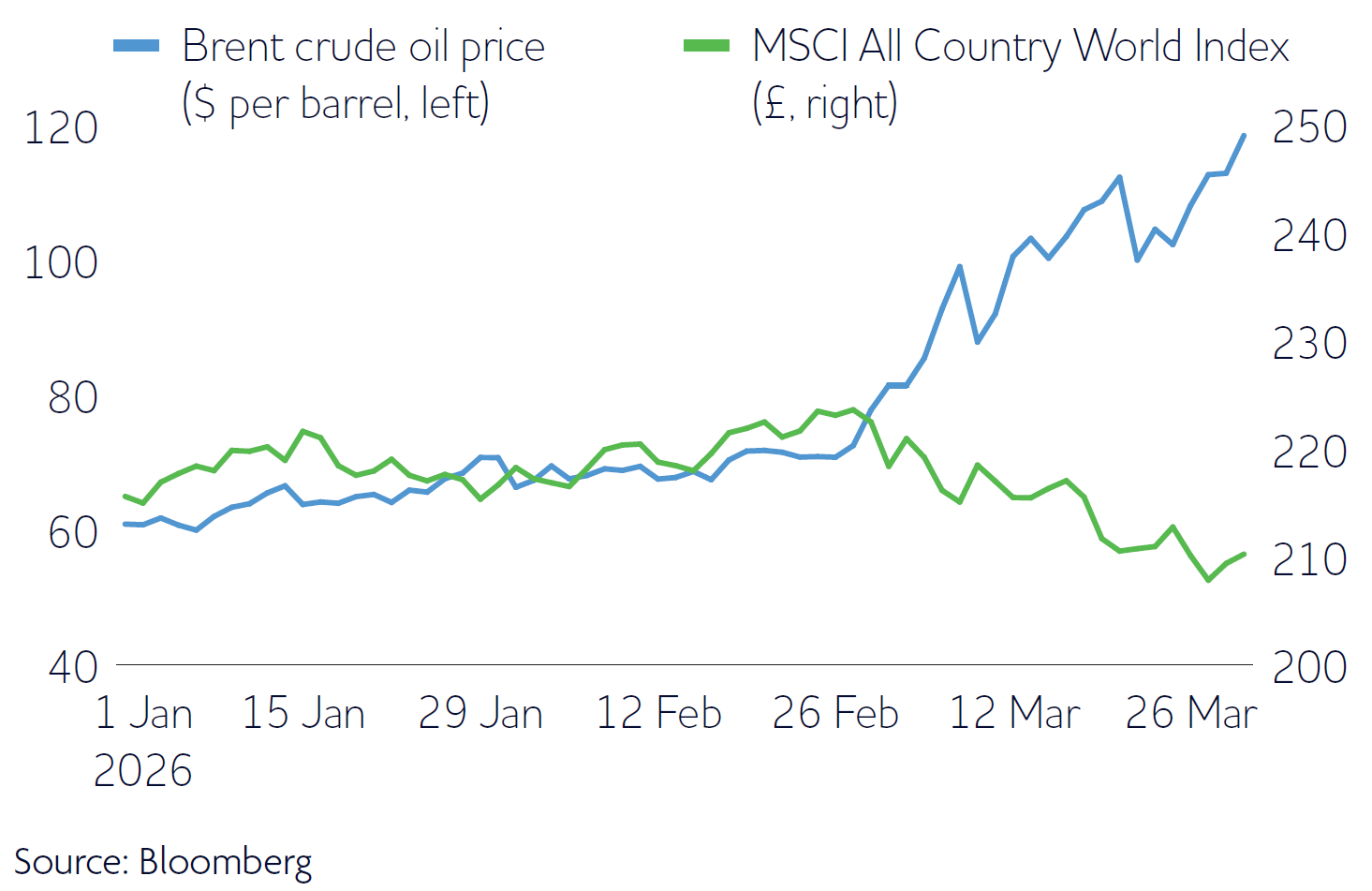

Figure 1: Markets are unsettled

Higher oil prices are likely to drag down economic growth and global stock markets have fallen in response.

Download Omnis Market Update (pdf)