To Track or Not To Track? That is the Question

Tim Dingemans, Investment Strategist here at Omnis Investments, discusses the ups and downs of Tracker Funds and why active management still has a key role in investment strategies.

To track or not to track? That is the question.

Tracker funds have been one of the biggest investment success stories of recent years. Assets under management have surged – so much so that, by some measures, more money now sits in trackers than in active funds.

Why? Two simple reasons: cost and performance.

- Cost: Trackers follow an index by design. No stock picking, no tactical positioning, no “value add”, just replication. That simplicity drives significantly lower fees, a key part of their appeal.

- Performance: For the past 15 years, global equity markets have been in a sustained bull run. Corrections have been relatively shallow and short-lived. In that environment, staying fully invested with no need for fine tuning has worked very well.

So, if trackers are cheap and have delivered strong returns, what is there to debate?

Quite a lot, actually.

The part we often overlook

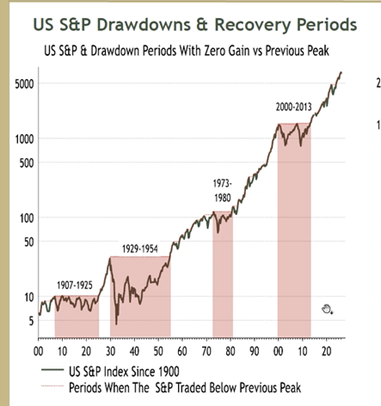

The last 15–20 years have been highly supportive of long-only strategies. But history offers a more cautious perspective. Had you invested at the market peak in 1907, 1929, 1973 and 2000, here’s how long it took for the market to recover.

Source: Absolute Strategy Research 2026.

How many investors can tolerate a decade or more just to break even?

This is admittedly simplified, and doesn't necessarily mean you should avoid investing at market highs, as timing the market is incredibly difficult. But the point is clear:

With a tracker, you capture all of the upside… and all of the downside.

A tracker fund should arguably come with a health warning: no additional effort will be made to preserve your capital.

Is there an alternative?

Over the long term, trackers often win on cost. But when downside risk matters, active management has a role.

An active approach aims to:

- Adapt portfolios - increasing exposure to areas expected to outperform, reducing exposure to expensive areas/areas expected to underperform.

- Limit losses in downturns, preserving capital for recovery

- Add value selectively - with the real benefit often being risk management rather than outright outperformance

Put simply:

A tracker can do nothing if the house is on fire. An active manager can at least move the furniture.

You might argue that these are extreme examples, but over time buying value rather than expensiveness has generally led to better outcomes. In the past, some friends and I set up an Emerging Market (EM) fund to take advantage of very cheap EM fixed income assets in 2009. Over time that cheapness corrected, and as a result our clients saw excellent returns. The active choice of the best value assets enabled us to outperform the broader EM indices.

Why this matters today

We may be approaching another inflection point.

The S&P 500 is increasingly concentrated, with returns driven by a narrow group of AI-led stocks. Index construction means this concentration could increase further if markets continue to rise, despite stretched valuations.

We contacted each of our underlying managers to understand the environments which are conducive - and not conducive - to active management. Almost all of them highlighted excessive concentration as a challenging backdrop.

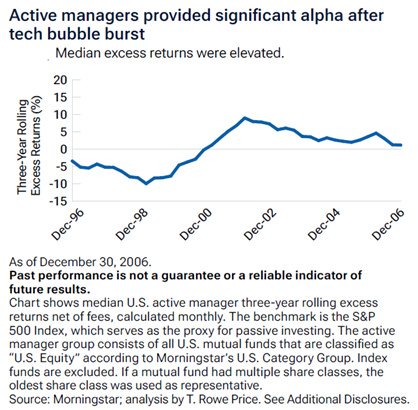

Narrow market leadership rewards highly concentrated positioning, which runs against the logic of diversification. History suggests that as we move out of highly concentrated markets, active managers have typically performed well – this is depicted in the chart below provided by Omnis investment partner, T. Rowe Price.

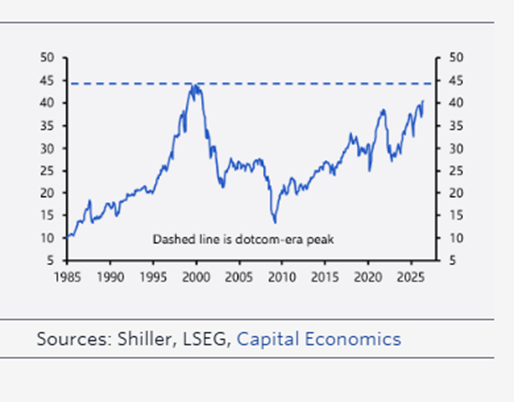

Valuations Revisited: Near Dot-Com Highs

Source: Capital Economics. Cyclically Adjusted Price/Earnings Ratio (Shillers CAPE)

None of this necessarily signals an imminent correction, but it does suggest that outcomes from here may be less straightforward than they have been in recent years.

Right now, I feel there is value in taking a more nuanced approach and trying to mitigate some of those risks - i.e. not relying solely on a tracker but incorporating a managed solution.

The Omnis Agility range does exactly that:

- We broadly follow the indices within a multi-asset, diversified portfolio across equities, fixed income and alternatives.

- Crucially, we actively manage those allocations to optimise the portfolio for the period ahead.

- Reducing exposure to expensive US equities and pivoting to better value assets makes sense.

What's past is prologue

Don’t assume the last 15 years define the next 15.

An active portfolio tries to avoid the worst excesses of the market, which can lead to smoother returns and less short-term pain than simply following the index.

However, if you’re comfortable taking on pure market exposure, it’s worth considering our strategy built on a carefully designed Strategic Asset Allocation process (Our new Access Tracker Funds), which can help manage risk more effectively and potentially avoid some of the pitfalls associated with purely passive approaches.

For those who want a more smoothed journey, a little bit of insurance (from Agility Funds) in your investment process should help you sleep at night.