Moving from US Equities to Government Bonds

Why are we reducing our US equity holdings and reinvesting the proceeds into a range of Government bonds?

A failing canary in the coal mine?

Author: Tim Dingemans - Investment Strategist

Last week, we reduced our US equity holdings and reinvested the proceeds into a range of government bonds.

We have been modestly underweight US equites for some time, so why now did we move further underweight?

As highlighted earlier in the month, one key area of concern has been the potential bubble in AI, which has so far been sustained by billions of dollars of investment from US big tech. Whilst cash flow has been more than enough to fund capital expenditure so far, the readiness of several key AI/tech companies to borrow, coupled with a potential US$800 billion shortfall in cash flow by 2030* raises further question marks as to the true ability of these companies to fund this expenditure.

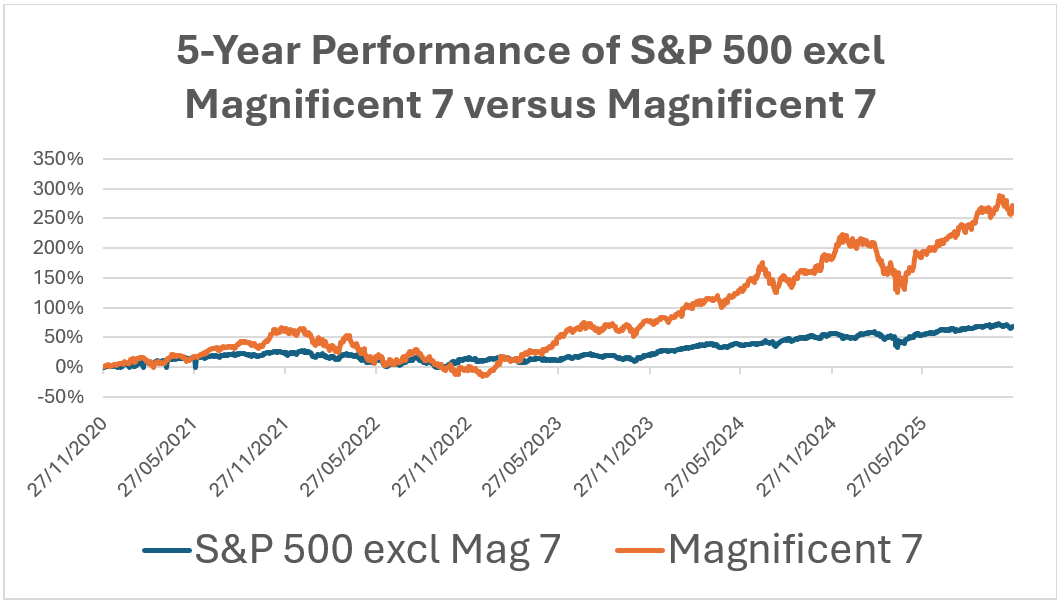

The US equity market has also become incredibly concentrated in a small group of tech stocks known as the “Magnificent 7” (Apple, Microsoft, Alphabet, Amazon, Meta, Tesla & NVIDIA) and no longer offers the diversification one might expect from holding a basket of 500 companies i.e. the concept of the index being a cross section of American companies across a range of industries is just not currently true. It means investors in the S&P 500 index are very exposed to a tiny universe of US tech giants.

Coupled with this, the financial plumbing in the US has started to clank. The cost for US banks to borrow from the US Central Bank (Federal Reserve) saw some pressure recently. This has at times been a good early indicator of less cash being available to the banking system. Additionally, more people are falling behind on their car loan payments. These are concerning signals, as tighter money and less loans are not good for economic growth, corporate earnings and by default the US stock market.

Whilst the US economy remains strong and corporate earnings remain robust; the vigour appears to be waning somewhat. Unemployment seems to be creeping higher and consumer confidence is falling. The US Central Bank (Federal Reserve) seems less confident surrounding near-term interest rate cuts, as forecasts for inflation remain sticky and still well above the Federal Reserve’s 2% target. Through our process of bringing together the large range of different factors mentioned above, we are seeing increased indicators that the US equity market looks ready for some form of consolidation or even correction.

At the same time, we have seen a pullback in French bonds amid rising political fears, while in the UK we have observed increased volatility in Gilts in the lead-up to yesterday’s budget. This has seen more attractive yields (which move inversely to bond prices) in both France and the UK. While returns from European bonds and US treasuries are also screening attractively. Bonds are generally considered safer than stocks and can provide steady income.

In summary, our investment analysis uses a structured, qualitative and quantitative process to assess a range of indicators. It combines country government analysis, macroeconomic data, company earnings and momentum indicators that we bring together via a process of consilience (the principle that evidence from independent sources can converge to strong conclusions). This summation of these various indicators provides a key step in our investment process.

Collectively, these factors combined over the recent period to green light a modest pivot out of US equities and into a basket of government bonds.

So finally, what next? Broadly, our concern is that these underlying headwinds of tighter money and overvalued stock markets will persist and quite likely start to be reflected in declining US stock prices. Should our investment process and indicators allow, we may well reduce US equity exposure further whilst increasing bond exposure.

So, we really do wonder if we are seeing a failing canary in the proverbial coal mine.

*Bain Technology Report 2025